Share

Published on 04 December, 2018

| Last Updated on 12 June, 2026

If you run an online business, you have almost certainly come across the terms payment gateway and payment processor. They sound similar, and most articles lump them together. But they do very different things, and understanding the distinction can save you real money and integration headaches.

This guide explains exactly what each one does, how they fit into a real transaction, and how to decide which combination makes sense for your business.

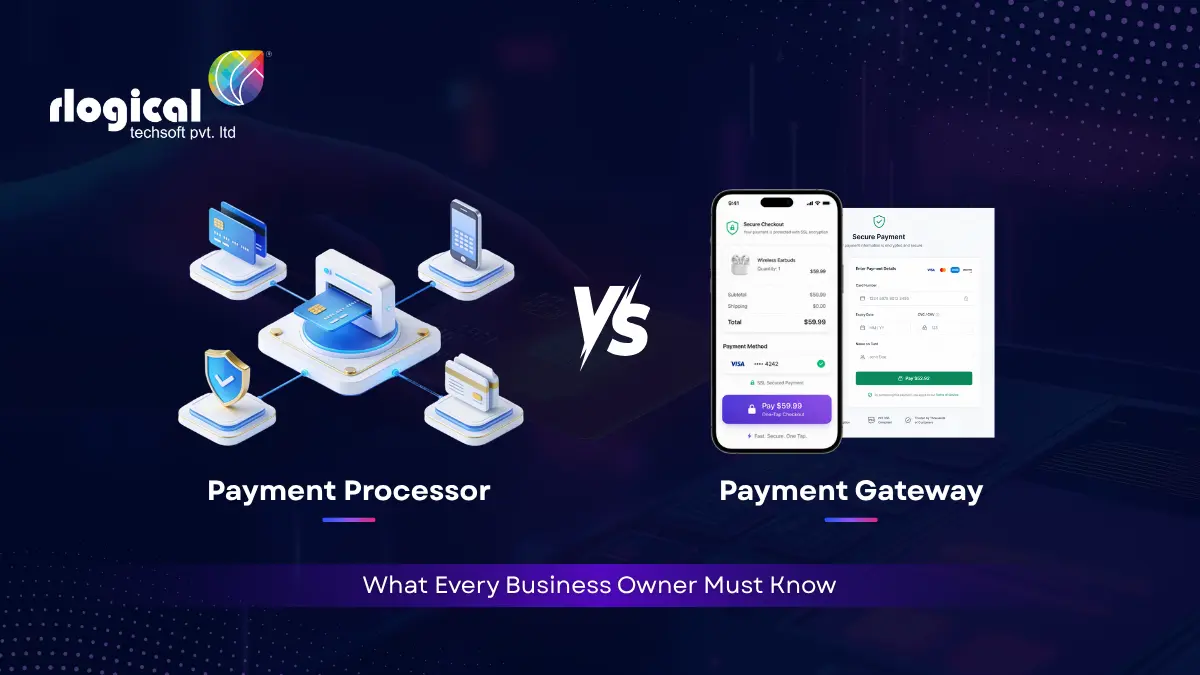

A payment gateway is the technology that sits between your customer and the financial system. When a shopper enters card details at checkout, the gateway encrypts that data and forwards it securely to the payment processor. Think of it as the digital equivalent of a card reader at a physical store.

The gateway handles two things above all else: data security and authorization routing. It encrypts cardholder information using TLS 1.2 or higher and AES-256 encryption before the data ever leaves the customer’s browser. It then tokenizes the card number, replacing the 16-digit Primary Account Number (PAN) with a randomly generated token that is useless to anyone who intercepts it.

For e-commerce merchants, the gateway is the piece your customers actually interact with. It is the secure payment form on your checkout page.

For businesses planning mobile payment integration, understanding the implementation process across different platforms is equally important. A detailed breakdown of payment gateway integration for both iOS and Android applications can help businesses make informed technical decisions.

Read More:

https://www.rlogical.com/blog/how-is-adding-a-payment-gateway-in-ios-and-android-applications/

A payment processor works entirely behind the scenes. Once the gateway sends it the encrypted transaction data, the processor takes over. It communicates with the card networks (Visa, Mastercard, American Express, Discover) and the issuing bank to verify the transaction and authorize or decline it.

The processor also handles settlement, the end-of-day process where all authorized transactions are finalized into a file and funds move from the customer’s bank to the merchant’s account. Different processors have different timelines for this, so if cash flow matters to your business, settlement speed is worth comparing.

Here is what happens in the two to three seconds between a customer clicking Pay and seeing a confirmation screen.

| Feature | Payment Gateway | Payment Processor |

| Role | Customer-facing data capture and encryption | Behind-the-scenes authorization and settlement |

| Primary function | Securely collects and routes payment data | Communicates with banks and card networks |

| What it handles | Encryption, tokenization, authorization routing | Card network messaging, fund movement, chargebacks |

| Typical fees | Monthly fee or per-transaction fee | Per-transaction percentage plus interchange fees |

| Integration point | Your website, app, or POS terminal | Works in the background; no direct merchant UI |

| Examples | Authorize.Net, Stripe (gateway layer), Braintree | First Data (Fiserv), TSYS, Stripe (processing layer) |

| Security standard | PCI DSS compliant, TLS encryption, tokenization | PCI DSS compliant, fraud detection, chargeback management |

For most online businesses, yes. The gateway handles what happens on your side of the transaction. The processor handles everything that happens at the bank and card network level. They work together in sequence, not as alternatives.

That said, the line has blurred significantly. Many modern platforms bundle both functions into one product.

If you are building on a custom stack or working with an enterprise setup, you may choose a standalone gateway (like Authorize.Net) and pair it with a separate processor. This gives you more control over fees and switching flexibility but requires more integration work.

Both components are required to meet PCI DSS (Payment Card Industry Data Security Standard) compliance. As of now, PCI DSS 4.0 requirements are mandatory, including stronger authentication, enhanced security monitoring, and tighter controls around script management on payment pages.

Tokenization in particular has become central to reducing PCI DSS compliance scope. When the gateway replaces the PAN with a token before the data enters your servers, your internal systems never touch raw card data. This shrinks the number of environments subject to PCI audits and reduces the damage of any potential breach.

Not all gateways integrate the same way. Understanding the options helps you balance security, user experience, and development effort.

The customer is redirected to the gateway provider’s secure page to enter card details. Your servers never touch the card data, which significantly reduces your PCI scope. Suitable for businesses with limited development resources. Examples include PayPal Standard and older Authorize.Net hosted forms.

The checkout form lives on your website, and card data is submitted directly through the gateway’s API. This gives you full control over the user experience but requires stricter PCI compliance on your infrastructure. Stripe Elements and Braintree’s Drop-in UI use a hybrid of this model, where a JavaScript library handles data collection client-side so raw card data never reaches your servers.

Pre-built libraries provided by the gateway handle secure card data collection in your web or mobile app. The SDK exchanges the card data directly with the gateway for a token, and your application receives only the token. This reduces PCI scope considerably compared to full API integration and is the standard approach for mobile payment forms.

The market has matured considerably. Here are the platforms businesses rely on most, along with what each one is best suited for.

Stripe remains the go-to for developer-driven businesses. It functions as both gateway and processor and supports subscriptions, marketplace payouts via Stripe Connect, multi-currency transactions, and a wide range of local payment methods. Standard pricing is 2.9% + $0.30 per transaction in the US, with custom pricing available at volume.

PayPal holds around 45% global market share for online payments as of 2026. Its strength is consumer trust. A large portion of online shoppers already have PayPal accounts, which reduces checkout friction. PayPal acts as both gateway and processor and integrates quickly, making it a practical first choice for new businesses.

One of the longest-established standalone gateways, Authorize.Net is widely used by merchants who want a reliable gateway they can pair with their own acquiring bank relationship. It supports virtual terminals, recurring billing, and a customer information manager for storing tokenized card data.

Square is strong for businesses that need unified in-person and online payment acceptance. Its hardware and software ecosystem is tightly integrated, making it a practical option for retail, restaurants, and service businesses that sell through multiple channels.

For businesses operating in India, Razorpay is the leading payment platform. It supports UPI, NEFT, RTGS, credit and debit cards, net banking, and wallets. It is PCI-compliant, offers developer-friendly APIs, and has expanded its presence to Singapore, Malaysia, and the United States.

Adyen is an enterprise-grade platform that consolidates online, mobile, and in-store payment processing on a single system. It is used by large global businesses that need a unified view of payments across markets and channels. Adyen negotiates interchange-plus pricing directly, which can significantly reduce costs at high volume.

There is no universal answer. The right choice depends on your transaction volume, technical resources, geographic markets, and the payment methods your customers prefer.

Before committing, test in sandbox mode. Most platforms offer this at no cost. Check settlement timelines, evaluate chargeback handling processes, and confirm that the gateway supports the card types and regional payment methods your customers actually use.

Choosing the right payment infrastructure requires balancing security, transaction costs, scalability, and user experience. Businesses should evaluate providers carefully to ensure the solution aligns with their long-term growth goals.

Learn More:

https://www.rlogical.com/

A payment gateway and a payment processor are both essential parts of accepting card payments online. The gateway handles the customer-facing, security-critical task of collecting and protecting card data. The processor handles the behind-the-scenes work of talking to banks and moving money.

Many modern platforms package both into one, which is often the most practical choice for businesses that want to move fast. But knowing what each component does gives you the foundation to evaluate platforms clearly, ask the right questions, and make changes confidently as your business scales.

Need help integrating a payment gateway into your web or mobile app? The right architecture from the start saves significant rework later. Whether you are choosing between Stripe, Razorpay, or a custom processor setup, getting the integration layer right matters as much as the platform you pick.

Every business has unique payment processing requirements. Consulting with experienced payment integration specialists can help streamline implementation, improve security, and reduce future development challenges. Working with a trusted development partner can also help you select the most suitable payment solution based on your business model, target audience, and long-term growth objectives.

For personalized guidance on payment gateway integration, mobile app development, or custom payment solutions, feel free to connect with our experts.

Contact for More Information:

https://www.rlogical.com/contact/

Rahul Panchal is a visionary technology entrepreneur and the Founder & Managing Director of Rlogical Techsoft Pvt. Ltd. Passionate about the power of Artificial Intelligence, he focuses on helping businesses transform through AI-driven solutions, intelligent automation, and data-centric digital ecosystems. Alongside AI, his expertise spans scalable web and mobile platforms, Cloud, IoT, and modern enterprise technologies enabling organizations to innovate faster, optimize operations, and build future-ready digital products with real business impact.

Global insights on technology trends, best practices, and digital transformation strategies.

A proven track record of high-impact deliveries across industries and technologies

Share with us. We'll assess its feasibility, suggest the right tech stack, and share a clear cost & timeline.

Years of Experience

Projects

Countries

Engineers

Verified Client Reviews

Industry Served